I wanted to let you know, I have now started a You Tube channel to add to the blog! Watch the first video below!

I’m really excited about this because I like making videos and I find it’s a little easier to entertain through video than through writing.

I’ll be attempting to post videos on Mondays and Fridays. We’ll be covering a lot of budgeting tips and strategies as well as all other things personal finance.

We’ll talk debt, savings, investing, and much more. This is all in an attempt to provide you more value as we move into 2021.

I uploaded a new video this morning where we break down a budget into its recommended percentages. Give it a watch and a like if you find it provides value to you!

Also, subscribe and hit that notification bell to keep up with the videos. It’s an excellent way to support me as I continue to work on content for you all.

April 15th is a bad day for paperwork (and accountants) but a lot of people seem weirdly excited for the results of tax day, don’t they?

“I’m getting a huge tax return this year so I’m going to use it on that trip to Europe I’ve been wanting to take!” I get it, I love getting a huge tax return as much as the next guy!

Here’s what’s funny. We are getting excited about a perception. We perceive that we are getting this huge payday once a year and it feels soooo good, but consider this.

The money your company withholds too much of is the equivalent of you giving the government a 0% interest loan for an entire year.

Last year we got nearly $3,000 back (partly due to some educational credits on Bailey’s part for college courses) which was sooo nice since we were preparing to purchase a house. But that was $3,000 that I could have been collecting my own interest on throughout the year.

What are you missing by not changing your withholdings?

My interest rate for my savings account is about 0.5%. This means that on $3,000, I could have earned $15 in interest (give it up for free money!). And that’s about a third of the interest rate I was looking at a year ago. Better yet, if I invested that money in a Roth IRA, I could have made somewhere between 7-12% ($210-$360) in interest. What could you do with $15? Or $210?

Are you like many people and enjoy optimizing your money? Do you use credit cards for the points you’ll earn? Do you switch bank accounts so you’ll receive an extra 0.2% return on your savings?

My point is this: optimizing your earnings by getting a higher interest rate should be no different than optimizing your withholding tax so you take home everything you can without paying anything extra to the government the following year.

A $0 tax return means you made the most of the money you have.

If you want to optimize your money, go to the HR person at your company and request some help determining how much you need saved back so your return next year is near $0. It’s not as fun on April 15th, but it’s much more fun throughout the year. I would change my taxes any day if it meant I could earn an extra $210 for doing it.

I like tax refunds so I get why people want to ensure they have a lot of money coming back to them every year. But consider what you may be missing!

Like what you read? Give me a follow in this little box below.

Have you ever received a job promotion or a raise and thought “Oh sweet, now we can eat out more frequently!”

I have!

Just a year ago, Bailey was in school and working very part time at a local mall. We lived frugally so we could save for a house and tuition at the same time.

When she graduated, we bought a house! Ok, quick pic because it makes blogs more interesting.

Our little fixer upper after we replaced the roof ourselves with so much help from friends. Never. Again.

And got a second income! And we dropped the tuition savings since she graduated. Suddenly our income and expenses were changing…

Careful…

And that’s where lifestyle inflation kicks in. Suddenly, we had a much larger income. We increased our restaurant fund. We increased our blow funds. We increased our miscellaneous fund among many others.

Now, to be clear, we lived very frugally while Bailey was in college. Our monthly restaurant fund was literally $30. Same with our individual blow funds (fun money). I’m not saying all lifestyle inflation is bad. If we kept going the way we were going, we would have gone crazy because we didn’t spend much money on fun stuff.

What I am saying is lifestyle inflation can cause you to lose out of significant savings opportunities if you aren’t disciplined. That’s why so many lottery winners lose all their wealth within a few years. It’s tough to control your desire for bigger and better houses and cars if you suddenly have an increase in cash.

So how do you avoid this? Let’s look at some practical ways to control lifestyle inflation.

How to control lifestyle inflation when given a promotion or raise:

Here’s the video version for those less inclined to the written word!

1. Give yourself a little slack (budgeted slack).

This may seem counterintuitive but here it goes — give yourself a little, tiny bit of slack. I mean, allow yourself a little lifestyle inflation just to reward yourself for the increase. But not too much.

This could be anything from giving yourself a little more budgeted money in your restaurant fund, blow fund, or something else that’s fun.

I think giving yourself this extra little bit of flexibility will actually help you be more disciplined with the rest of your money. I talked about this in my post about blow funds.

I believe with all my heart that Bailey and I spend less money overall because we have a budgeted amount of money each of us gets to blow on literally anything each month. It helps curb our spending because we know we’re allowed to let loose just a little bit.

2. Make a budget!

Speaking of a budget in the first point, make one! Budgets don’t sound fun but they aren’t what you think. People think budgets restrict their spending and thus restrict their fun. But what people don’t realize is a budget is far more freeing because you’ll know EXACTLY what you can spend! And it gives you permission to spend it.

With a budget, you’re more likely to be responsible with how you spend the money at risk of lifestyle inflation. For one, if you get an extra $200 a month as a raise, it’s really easy to say “Well, I’ve got $200 more now. Of course I can go out to eat with my friends again!” Budget that money when you aren’t weak-willed and when temptation arises, you’ll be ready.

3. Put it towards debt!

The easiest way to control lifestyle inflation is to make the money disappear quickly before you have the chance to spend it. Do you have consumer debt? Throw that extra cash at your debt! Pay it off as fast as you possibly can and you won’t owe anyone anything. It’ll feel so good. Your income, your greatest wealth-building tool, will not be absorbed by any payments.

And that will change your financial life.

4. Start/increase your retirement savings!

This is my personal favorite. This one can be done so that you never even see that extra money. With making a budget, you have to control your desire to spend that money on frivalous things. When you’re thinking about paying off debt, you have to force yourself to send in that payment.

If you start a retirement account (Roth 401k or Roth IRA), you can immediately start saving that money before it hits your checking account. When I got my last raise, I increased my retirement savings to 15% in my 401k. That money was pulled out before I got my paycheck. Lifestyle inflation controlled.

One thing to note: I wouldn’t do this if I had consumer debt. Pay that debt off first. And don’t get any more consumer debt after that. Then get a 3-6 month emergency fund. THEN increase your savings.

5. Automate savings

Similar to the last point, set up automatic withdrawals from your checking account into a savings account. You can do this so it automatically happens every payday.

Automating your savings will help you save for the car you want (no payment!) or the house down-payment or even that big vacation you want to take without paying it off for months to come.

You can control your money

Going back to lottery winners, those who blow their wealth always regret it. You may be given a much smaller increase in income but I’m confident you want to avoid any regret when it comes to your money.

What are you going to do with that next promotion or raise? I want to hear from you in the comments below!

Like what you read? Give me a follow in this little box below.

What am I saying, I’ve got a huge project due at work today. Well, I hope you are having a happy Monday.

Regardless, thanks for joining me. I don’t take a single reader or follower for granted.

Alright, let’s talk money myths. Last year, my cousin and I were talking about money while we were playing tennis. Naturally. My cousin is financially savvy, very in-the-know when it comes to money speak.

Taxes came up and she mentioned that she and her husband were trying to keep their income below a certain point to avoid the bump in overall taxes. She said they didn’t want to make less money just because they entered a higher tax bracket. I was confused because that’s not how tax brackets work.

This was a simple misunderstanding, certainly nothing against her. But if a financially savvy individual doesn’t understand how tax brackets work, how many other people is it incredibly confusing to?

Let’s break down tax brackets

Alright, let’s do this!

Tax brackets are broken down into levels of income and corresponding percentages paid in tax to the federal government. There are more categories than this but we’ll show the most common, single or married and filing jointly.

Single Filer Tax Bracket

Married Filing Jointly Tax Bracket

Here’s the myth

Now that you have the IRS tax brackets for 2020 in front of you, it’ll be easier to understand what I’m talking about. Here’s the myth that many people including my cousin believe.

Myth: If I’m married and filing jointly, we’ll be paying 22% in taxes instead of 12% if we make even $1 more than $80,250.

If this couple made $80,250, the myth would say that this couple would pay $9630 in taxes (12% of $80,250). This would leave them with $70,620. And if they made $80,500, they would pay $17,710 (22% of $80,500). This would leave them with $62,790.

If this were the case, you can understand why this couple would want to avoid the extra $250 of earning. It would save them $8080 in taxes and come home with more money, clearly worth losing the $250 of extra income!

Here’s the bust

Here’s how it actually works. Let’s take the same couple making $80,500.

First they would pay 10% of the first $19,750. That’s $1975.

Next they would pay 12% of the amount over $19,751 but under $80,250. That range is $60,499.

That means they would pay 12% of $60,499. That’s $7260.

Then they would pay 22% of anything over $80,251 but under $171,050. Since they make $80,500, we only care about the $249 over $80,251.

So they would pay 22% of $249. That’s $55.

Given their income, they fit into the 22% tax bracket but they don’t pay 22% on their full income.

To figure out their final tax bill, we take the $1975 from the 10% bracket, the $7260 from the 12% bracket, and the $55 from the 22% bracket and add them together.

They would owe the IRS $1975 + $7260 + $55 = $9290

I hope you now understand how relatively simple tax brackets really are! And I hope you won’t worry about making more money because you won’t lose more money in taxes than your increase in income.

In the case of our lovely couple, their last $249 was taxed at a higher rate of 22%, but they still came away with $194 more after tax than they would have if they didn’t make that extra money!

Long story short, if you get the opportunity to make more money, do it. You won’t come out financially any worse than if you didn’t.

Today, I’m going to share with you something about which I’m very passionate! When it comes to helping people get out of debt and get ahead with their money, it’s hard to beat the Baby Steps.

What are the Baby Steps you ask? It’s what millions of people worldwide will attest to helping them get control of their money. It’s what Dave Ramsey put together about 25 years ago as he worked his way out of financial ruin.

Here’s the video version for those more inclined to the spoken word!

It’s what my wife and I have been following for the three years of our marriage. And it works.

Now, without wasting time, let’s get an overview of the Baby Steps to start! Then we’ll go a little more in depth on each one.

The 7 Baby Steps

Baby Step 1: Save $1,000 in a beginner emergency fund.

Emergencies are a part of life, whether we like it or not (we don’t)! That’s why you need an emergency fund! You’re going to start out with $1,000. It might not seem like much but it will just be enough to get you by while you pay off your debt. Don’t freak out. Keep your pants on till step 3 at least.

Baby Step 2: Pay off all debt except for the house.

This is where your wild comes out! You’re going to pay off debt like there’s no tomorrow.

Or, uh, like there is a tomorrow and a collector is going to call you..

Anyway, the point of this step is to rid yourself of all non-mortgage debt. That means everything. How are you going to do it? Use the debt snowball.

The Debt Snowball

This is where you pay the minimums on all the debts you have except for the smallest one. Then you put all you possibly can towards paying off that smallest debt. Once that’s gone, you do the same with the next smallest one. When that’s gone, you do it on the next one.

It might not be the best way to pay off debt mathematically, but it will help you gain momentum which is what we care most about. Most people would think they should pay off the highest interest rate debt first. Ultimately, it’s up to you, but if you stick to the debt snowball, you will gain momentum and will knock it out. People do it all the time.

Baby Step 3: Save 3-6 months of expenses for emergencies.

This is where your finances get just a tad more comfortable! You already have your $1,000 emergency fund (presuming there wasn’t an emergency that happened within the last paragraph). Now just expand it to 3-6 months!

Make sure you don’t get confused here — it’s not 3-6 months of incomes, just expenses. Calculate your expenses for a month and just multiply it by 3 or 6. Now, this is going to depend more on you and your comfort level. Do you have consistent income or inconsistent income? Do you have a high or low risk tolerance? Choose how many months you want covered based on that.

Make sure you save this fund into a place you can get to it quickly. That means no investing with it. Just throw it in a high yield savings account and watch it grow slowly but surely.

Baby Step 4: Save 15 % of your income for retirement.

Did someone say retirement? Travel?

This step takes some extra self discipline because you have to be willing to give up a good chunk of your money to ensure you don’t have nothing in the future.

Wherever you work, go to your HR representative and ask about a retirement account. Most employers have them. If they offer an employer match, make sure you take advantage of it!

One thing to note: You want to be putting your retirement money into a tax-favored account. That means putting it into a Roth 401(k) and a Roth IRA. These will allow you to pay taxes on the money you contribute now, and then, when you retire, you’ll be able to withdraw the money plus all the growth at no tax rate.

Baby Step 5: Save for college for your children.

Some parents like to ensure their child never has any debt. Other parents find they prefer to teach their child the value of money by making them pay for everything in college. My parents did somewhat of a hybrid. It’s completely up to you.

Baby Step 6: Pay off the house early.

Don’t wait till the end of the mortgage! Throw some extra payments on that now as you are able. Make sure it goes straight to the principle. This will be your last EVER debt!

I am so unbelievably excited to pay off our house early. It’ll still be a while but I am motivated.

Also, just so you know, Baby Steps 4, 5, and 6 are to be completed simultaneously.

Baby Step 7: Build wealth and give.

Continue what you’re doing except now you can add more money into that retirement account! Maybe you want to start investing in real estate. Now’s the time!

And most importantly, give outrageously. Generous people are attractive people.

Do the Baby Steps Work?

Absolutely. They have worked for millions of people.

Here’s why I like the Baby Steps. Out in the world are gobs of people trying to help you hack your life financially. They’ll tell you about credit card churning, traveling on credit card points, etc. just to make a little extra cash. I like the Baby Steps because it’s simple. There are no if’s and’s or but’s. It works the same way for everyone, regardless of life circumstance, salary, etc.

And it’s a proven method that will work for you too.

I’ve been asked on a few occasions why I don’t use credit cards.

“I mean, you get points and cash back and if you pay it off, it isn’t a problem, right?”

Yes, true! I love rewards. I sign up for a lot of rewards programs to take advantage of saving money. And there are some tempting benefits to credit cards.

Here is the video version for those less inclined to the written word!

Credit Card Pros

Security: Credit cards have great security. If your card number is stolen and illegal purchases were made without you knowing, all it takes is a call to the credit card company to have it taken off your account. They’ll send you a new card and you’ll still have access to your money in your bank account.

Credit: Credit cards give you the opportunity to build credit so it’s easier to get loans if you need them.

Rewards: Credit cards allow you to get rewards on the money you spend on a regular basis whether that is through cash back or airline points.

Insurance: Credit cards can give you an extra layer of insurance on items you buy. Some provide some extra comprehensive insurance on a rental car, or maybe theft protection of items purchased in the last 90 days.

So why don’t I want to take advantage of these benefits? Do I just not see how I could make credit cards work for me?

I can see it. I really can. I’m so aware of my financial status, I could easily make the benefits work for me and make me more money.

That means the credit card companies are making billions upon billions of dollars from people who can’t afford to use credit cards.

Credit cards are heavily marketed in America. It’s pretty clear why. The companies make a ton of money off people who can’t pay them off every month.

I think everyone uses the excuse that credit cards are okay because you can just pay them off every month. But statistics show real life looks different than intentions.

Here’s Why I Don’t Use Credit Cards

I love talking money with people so much that I got training to be a financial coach from Ramsey Solutions. I want other people to enjoy the freedom of no debt.

The reason I don’t use credit cards is because I want to show people that they can live without them. Those who come to me for financial coaching are more likely to be those who need to quit using credit cards entirely to get their financial lives back in shape.

Those stats I showed above? People who need financial coaching are the ones paying over 15% in interest on their credit cards. Sure, credit cards carry some great benefits, but not for these people.

And I can’t in good conscience use credit cards while I tell other they shouldn’t. I can’t do it.

I don’t want someone who is deeply entrenched in credit card debt to say, “Well, Caleb uses credit cards and pays it off every month. I can do it too.”

I want them to say, “Caleb is proof I don’t have to use credit cards any more and he can support me in that decision.” That’s why part of Dave Ramsey’s baby steps involves cutting up the credit cards and never using them again. Credit cards are designed to make money for corporations, not you. So I want to support people who need to do this by not using credit cards myself.

Some Other Benefits to Ditching the Credit Cards

Personally, I’ve found a couple other reasons I don’t need to use a credit card.

Debit cards have similar security measures. I am on our checking account fairly frequently. If there is a fraudulent purchase, all I have to do is inform the bank as soon as I see it and they will take care of refunding me that money and sending me a new debit card.

I don’t need credit. I don’t like payments at all so I have committed to paying for everything with cash from here on out. Contrary to popular opinion, you actually don’t need credit to purchase a house. If you go with a company that does manual underwriting (like Churchill Mortgage), you can still obtain a mortgage with a great interest rate, no credit needed.

I find it is far easier for me to track my finances just based on using a debit card. I never have to wonder if I have enough money in my bank account to pay for my credit card bill because every time I purchase anything, that money is take straight out of my account. Seriously. I have to legitimately live below my means because if I don’t, I run out of money. I’m much more careful that way.

I Understand Why People Like Credit Cards but…

There are some nice benefits on the surface. I just can’t justify it myself with the type of financial help I want to provide to people.

I honestly don’t have a problem with people using credit cards. People will do what people will do. That doesn’t mean I wouldn’t encourage someone to get rid of credit cards if I had the chance. In fact, if I ever coach you in your finances, you can bet I’ll encourage you to cut them up. But money is such a sensitive topic, I don’t want to push people away because I’m giving them unsolicited advice on credit card use.

And I know that not everyone is the same. Many people pay for food on credit cards because they don’t have the money to pay for it any other way. If that’s you, please please please fill out this form below so we can talk about your situation. I promise to give you hope.

Do you use credit cards? Why or why not? I want to hear from you in the comments below!

What are you not going to purchase today? I want to know in the comments!

Black Friday is all about spending money and getting killer deals. I love me a good killer deal. I’ll probably get some today to be honest.

And by all means, get some Christmas shopping done or pick up that item you’ve been eyeing for a while. Just don’t go buy stuff for the sake of buying stuff.

I fear that many people are just like me in that it is so easy to make excuses for purchasing things when there are good deals. Black Friday is a PERFECT excuse for a spender like me. Though I’m more of an online shopper than an in-store one.

Amazon Prime, yo. ✌🏻

Regardless, if something is a good deal, it doesn’t mean you have to purchase it. We don’t want to steal from our future by frivolously spending money now.

If you are going to buy something today, go for it, but be intentional about it. Don’t make an impulse decision!

Now, tell me what you didn’t buy! Personally, I did not buy some new tennis shoes even though my current pair are wearing out. Let me know in the comments down below!

Budgets are daunting if you aren’t a numbers person. Just getting it set up for the first time is challenging. How are you supposed to know how much money to put into each category? What’s the “responsible” percentages? How to adult?

Below is a breakdown.

10% in Giving

10% in Saving

25% in Housing

5-10% in Utilities

10-15% in Food

10% in Transportation

5-10% in Medical/Health

10-25% in Insurance

5-10% in Personal

5-10% in Recreation

5-10% in Miscellaneous

Now, of course, these aren’t perfect for everyone. These are recommended percentages straight from Ramsey Solutions based on research and experience. Percentages are going to be different based on your situation.

If you have a higher than average salary, some of your categories are going to be much smaller! Like food in particular.

These percentages are a great place to start. Get started budgeting today and break down your spending into these categories. See what percentage you’re putting into each per month. How are you going to have to change your finances in order to hit these targets?

Here’s the video version for those more inclined to the spoken word!

Let’s look at an example

Let’s pretend you make $50,000 per year. After taxes, you would have about $3300 left per month. Let’s break this down so you can see exactly where you’d be at.

Giving: $330

Whether it is 10% of your pre-tax or your post-tax income, what organizations are doing important work in your eyes that you want to give to? Personally, Bailey and I are Christians and give to our church because we believe in it’s mission.

Giving is important because this is how you keep a healthy perspective of money. I know for me, it keeps my greed in check and reminds me that I’m merely a manager of the money I have.

Saving: $330

Ultimately, we want to get to a higher savings rate than 10%. This is a healthy start, though. Keep in mind, the goal is to hit 15% in saving for retirement. But if you aren’t used to saving, 10% is a great way to get you to that fully funded 3-6 month emergency fund.

Housing: $825

This means keep rent below this if you live in an apartment or a house. Or it means keep your mortgage payment at or below this including property taxes. We’ll cover insurance in a minute.

Utilities: $165-$330

Get your electric, gas, sewer, garbage and water below this all together!

Food: $330-495

Food is an important one and here’s why. Most people spend way too much on food!

People go to the grocery store with no plan, buy things they didn’t plan to buy, get name brand items when generic is almost identical, AND spend far too much eating out.

Food is a simple section of the budget where money can almost vanish without you realizing it. Keep your food budget in check!

Transportation: $330

This will include anything from gasoline to maintenance on your car(s).

For transportation, Bailey and I have two lines. One for gas and one for car maintenance. Maintenance is hard to factor in since it’s not a consistent monthly expense (some months, we spend absolutely nothing on maintenance even though our cars are 180k+ miles). However, if you start a sinking fund for maintenance, it’ll be ready to go when your car isn’t!

Health/Medical: $165 – $330

You’re going to get sick and bad things will happen so be prepared! Of course, insurance does take care of a lot of health and medical things, but you still need to pay for anything from doctor’s visits to medications to deductibles to bandaids. Maybe even bandaids with Olaf on them.

Insurance: $330 – $825

So much insurance!

Home insurance, renter’s insurance, auto insurance, life insurance, health insurance, identity theft coverage – it all counts. Shop around. Get an insurance broker who can shop around for you. They know the industry and can find the best rates while comparing all your options.

Personal: $165 – $330

This is Bailey’s and my favorite section of the budget. We call it the blow funds. I wrote about this recently and you can read it here.

What I love about the blow fund is it is designed to give you some flexibility in your budget. I am convinced that we spend less money on frivolous things because we have blow funds. Then we keep ourselves to a certain amount of personal money instead of spending far more money on a bunch of little justifications.

Make a personal category and let yourself splurge a little each month. Just don’t go overboard!

Recreation: $165 – $330

Here’s the section for any of those entertainment items like clubs, concerts or going to the movies. Though, you might be saving a little money in this category with current Covid restrictions!

Miscellaneous: $165 – $330

Last one. This is for all the miscellaneous items that come up throughout the month. For example, our dog, Jack’s collar broke and we have to purchase a new one! Or we need paint for repainting our living room.

How was I not expecting that?

Regardless, this all goes into miscellaneous. Plus, then it won’t screw up any of my other categories.

Wait! Before you make your new budget!

Here are a couple very important things.

This did not include paying off debt.

This is only a guideline.

If you are in debt, I recommend paying it off as quickly as possible. This means sacrificing some serious money in a lot of those above categories so you can make some progress on your debt payoff.

Check out Dave Ramsey’s Baby Steps in order to get some good direction on paying off debt and getting ahead financially.

Remember, this percentage breakdown is a guideline.

Not everyone’s percentages are going to be the same. Personally, our savings rate is a little higher because we’re preparing for some big home renovation projects coming down the line.

Also, remember you have to make your percentages add up to 100%. If you take the higher number from all of those category ranges, you’ll be over 100% and that’s a good way to go further into debt!

Budget is important. Don’t put it off.

The important thing is start budgeting today! A positive view of money starts with telling it where to go versus wondering where it went. There are lots of great apps you can use for a budget. Check out some that I think are great options here.

If you find you need more help getting your finances in order or even just getting a start on budgeting, shoot me an email at balefinancialcoaching@gmail.com or sign up for a free call below. I’ll coach you through paying off debt and making an effective budget! First session is always free. Start today, don’t way till tomorrow.

So how’s your budget looking? Are your percentages in the right place? Do you even have a budget? If you are in need of budgeting help, I’m happy to do a free budget review. Just contact me through my website and we’ll start getting you on the right track.

This week we covered a sinking fund. Basically, it’ just a section of the budget for setting aside a certain amount of money per month in preparation for a predictable expense. A couple examples we used were anything from Christmas savings to saving for a house or car. Today, we’re going to look at a type of sinking fund: The Blow Fund.

Here’s the video version for those less inclined to blog posts!

The Blow Fund

What is the blow fund? I actually took this term from our pastor when he mentioned off hand how he and his wife budget fun money. Each month, he and his wife get the same amount of money put into their blow fund. And each is allowed to blow their money on anything they want without having to talk to the other.

I liked that idea a lot when Bailey and I were engaged so we implemented it into our first budget.

$30 a month.

Not a lot but hey, one of us was in college. We had other expenses!

Since Bailey graduated, we splurged and upped our monthly blow fund money to $50 each. Okay, maybe it’s still not a lot.

Unlike a sinking fund for tires where you reach a goal and stop saving (like $600), the blow fund doesn’t leave the budget. Every month the same money is set aside for this. It can continue to grow. Last October I had $400 in my blow fund!

What about monetary gifts for birthdays and Christmas?

We actually put these in our blow funds as well. I know some people who don’t but my opinion is that, if someone gives Bailey a gift for graduating from college, it’s a reward for pushing through. I’m fine with her getting to spend that on something she likes. And if we get money for birthdays or Christmas, we put that in our blow funds too.

Some people handle that differently. This has worked well for us though.

Why a Blow Fund is Important

I assume you don’t need me to lecture you on why a blow fund is important.

“I’m just glad you are telling me to spend money on frivolous purchases!”

Yeah, pretty much. But there’s a lot more depth to a blow fund than that.

A blow fund gives you some space in the budget for buying something you couldn’t justify otherwise. It gives you permission to be a little irresponsible.

That permission is important because it’ll help curb those frivolous desires otherwise. Instead of thinking “Ugh, I can’t buy that because we have to be ‘responsible'” it’s more like “Oh, I could buy that with my blow fund. But if I do, I’ll have less blow fund for something else so maybe I shouldn’t.”

If you give yourself no space in your budget for fun money, chances are you will actually spend far more on frivolous purchases than if you budgeted for it.

Don’t Go Overboard!

This is where you have to be careful. Don’t. Go. Overboard.

You go overboard and you could drown. Financial drowning is no fun.

Bailey and I kept our blow funds at a minimum while we were on one income and she was in school. $30 each, that’s it.

Now, we’re up to $50 each. Overall, that’s not a lot. It’s a small percentage of our budget but it does give us just enough space to spend money on some fun things we couldn’t justify otherwise.

A friend of mine tends to go overboard with his blow fund. He budgets out every month for the necessities and he also budgets a blow fund. But if that particular month brings the desire to purchase a radio for his motorcycle helmet and there isn’t enough money in the fund, he shifts money around so he can put more in the fund. It happens every month pretty predictably.

I want you to understand a blow fund is a great tool but you have to control it. Keep it consistent, don’t throw more in your blow fund just because you have money. Every time that happens, it takes away from your other goals like retirement (or another sinking fund!).

What do we spend our blow funds on?

Recently, Bailey has been obsessed with Happy Planners. She got one and now has an addiction to purchasing stickers for it. Like, all the stickers. She has used her blow fund to purchase 20 books of stickers.

She has over 16,000 stickers.

But she has a blow fund. That many stickers wouldn’t fly if it were coming out of our normal budget. But she can spend it how she wants!

I, on the other hand tend to save up for technology or larger things in general. Last year, I bought a used iPad and a used Apple Watch. I haven’t regretted either purchase!

Financial Coaching Designed for You

As always, if you find you are in need of help, set up a time with me for free and we’ll talk your money and your goals. I’m a Ramsey trained financial coach and I love talking money and providing hope. Just set up a 30-minute call with me and I’ll listen to your situation and help you determine what needs to happen. My guarantee is if you don’t make progress, you get your money back. I promise the investment in coaching will give you payback many times over. And the first session is free.

Today we start a new series! We’ll be covering different categories of a budget to give you practical knowledge for starting or improving your own budget.

A budget is the building block of good finance. That is what will help you track your money and hit your financial goals.

The Sinking Fund

This is a fund created for anything that is predictable enough to save for. If it’s predictable, start a sinking fund for it.

One easy example is Christmas.

Christmas happens on the 25th of December every year! That’s the definition of predictable.

Creating a sinking fund for Christmas is as easy as this:

Start one in your budget.

Figure out how much you’ll spend at Christmas.

Divide that number between the number of months till Christmas.

Example Time

The average person spends about $900 on gifts at Christmas. Let’s say our average friend, Steve, didn’t thinking about Christmas until this month, October. Steve can create a sinking fund then budget $300 for it in October, November, and December and boom! Steve doesn’t have to shell out $900 in December because he prepared in October and November as well.

Better yet, our average friend doesn’t have to pay off that $900 in January because he wasn’t prepared.

Budgeting App: EveryDollar

This is my favorite budgeting app. It helps you budget by encouraging you to give every dollar a place. Then you won’t be spending “extra cash” on coffee or Chipotle because you have it. Every extra dollar is given a place so that you can reach your financial goals more quickly.

It’s harder to take money from your savings category if you want to eat out!

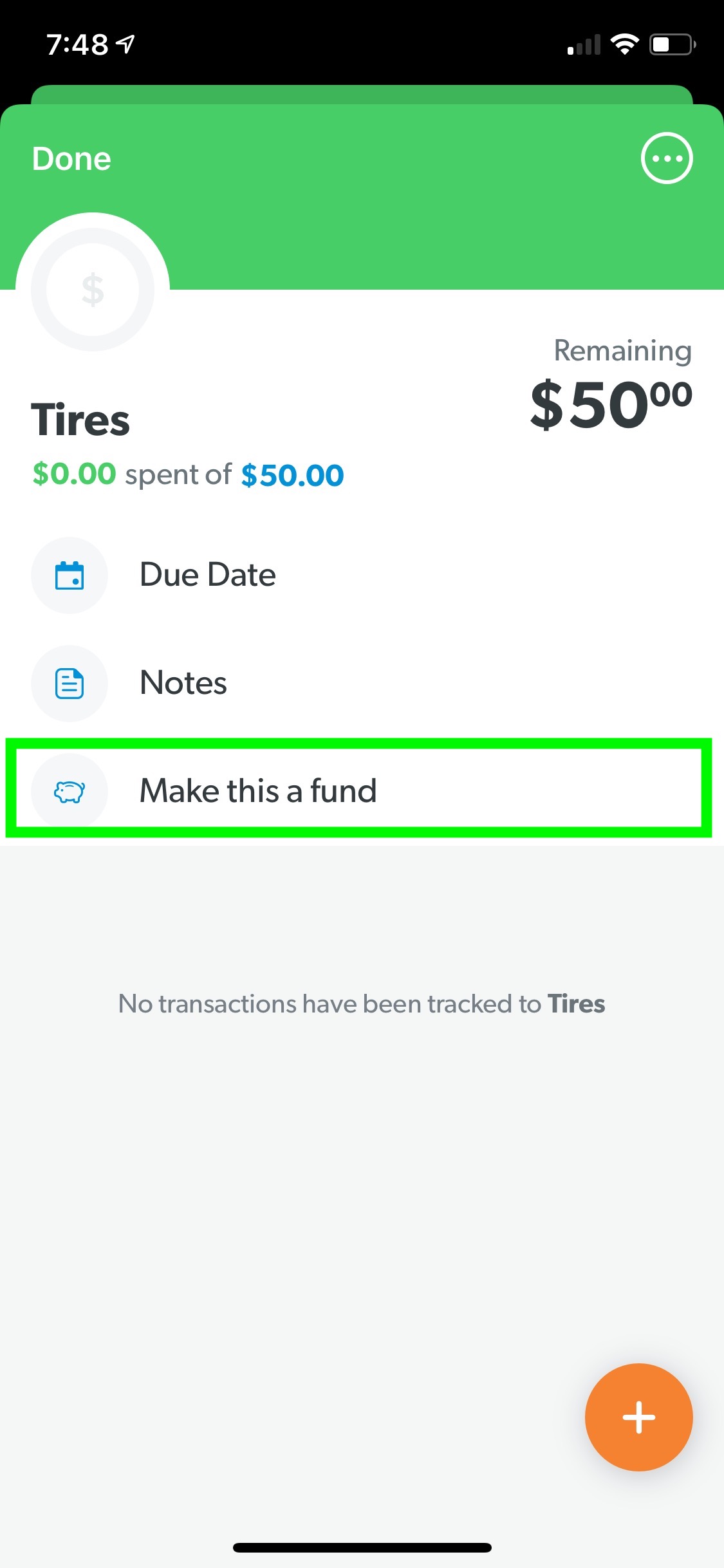

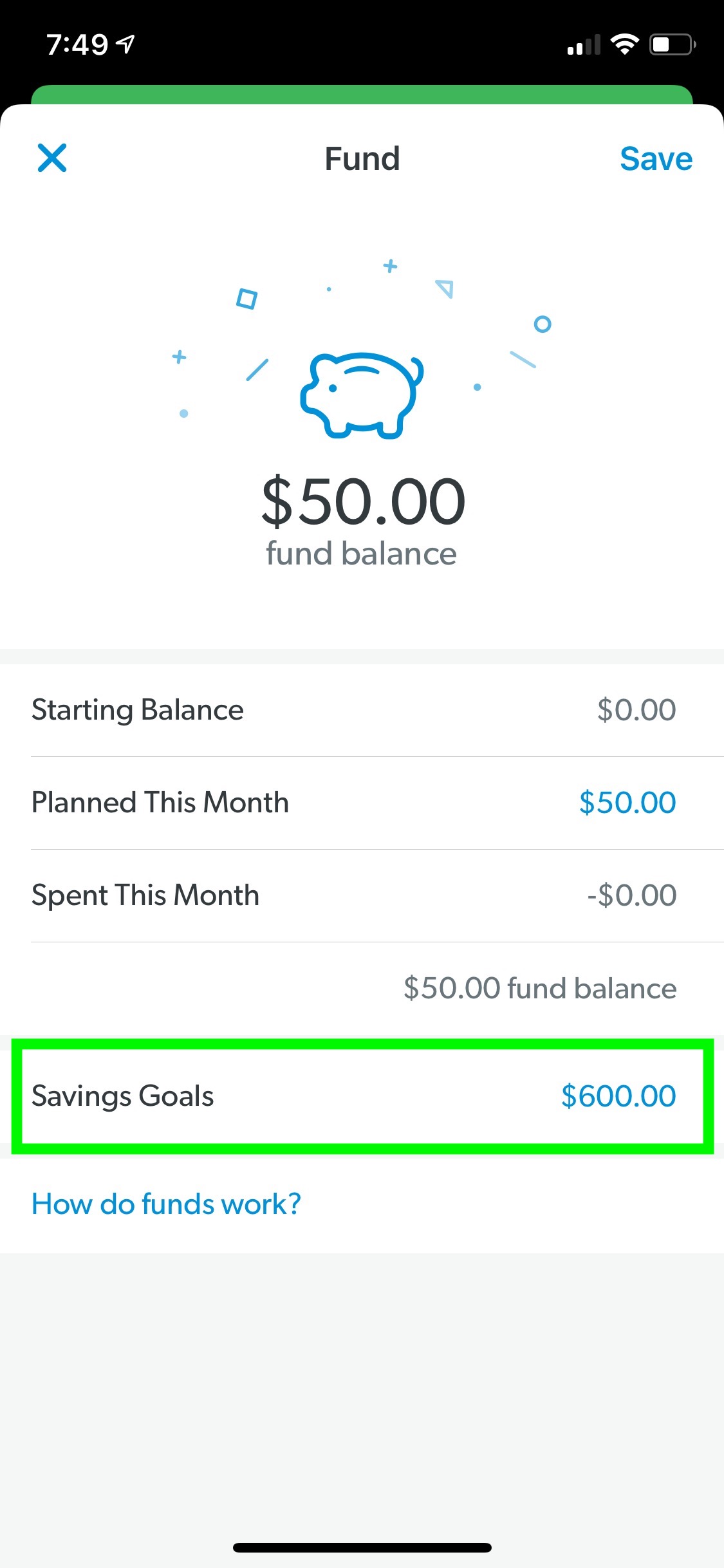

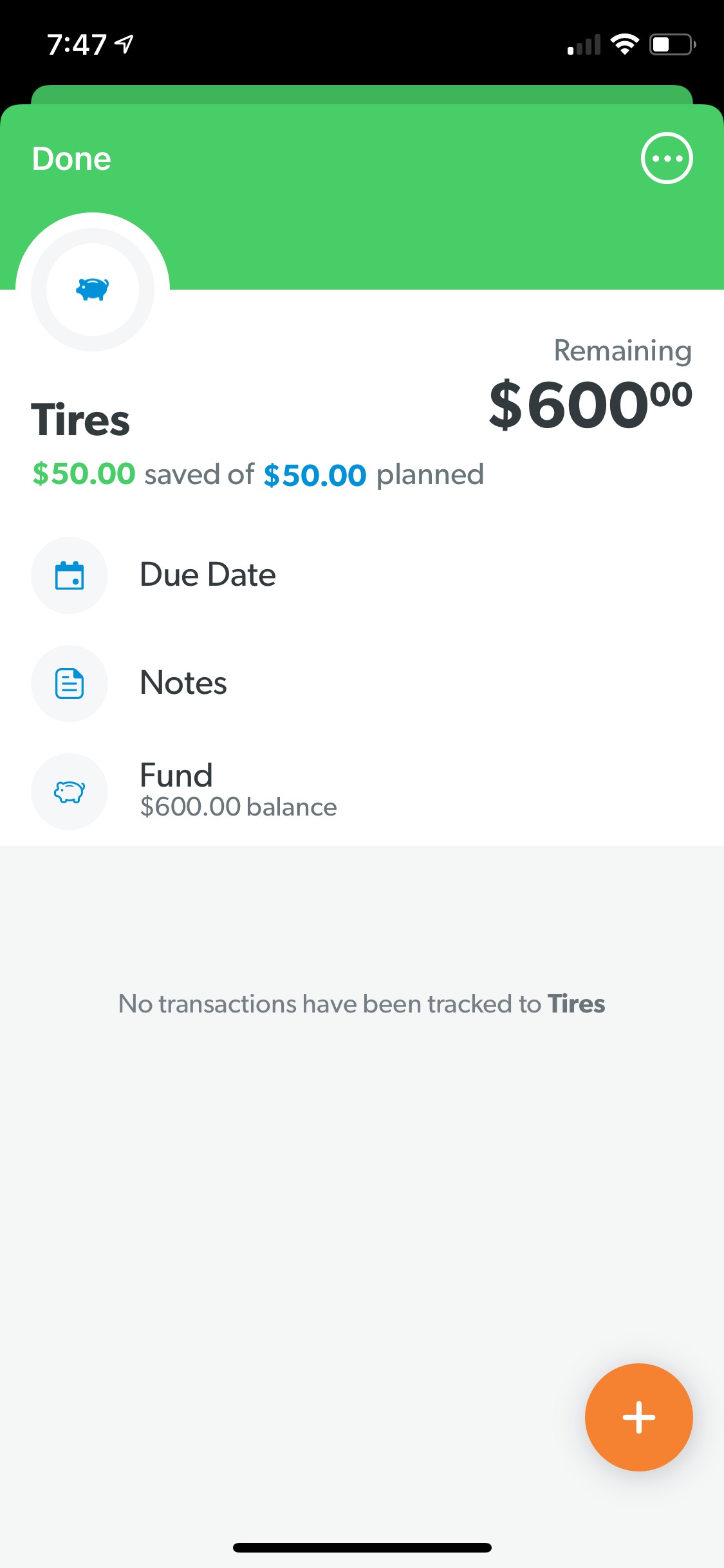

I have a sinking fund for new tires and here’s how to make it on EveryDollar.

In the first image, I created a new line in my budget and named it tires. I added $50 to the line. Then I selected “Make this a fund.”

In the second image, it shows instructions for how to use a fund for saving. I selected the blue “Make this a fund.”

In the third image, I set a savings goal of $600.

In the fourth image, I can see that after 12 months of saving, I have enough saved in a sinking fund for new tires!

Christmas is coming. Start saving today!

I hope you understand the importance of creating sinking funds. Christmas is coming, set one up today! Think through whatever else may need a sinking fund. Tires? A home downpayment? It works for anything.

Financial Coaching Designed for You

As always, if you find you are in need of help, set up a time with me for free and we’ll talk your money and your goals. I’m a Ramsey trained financial coach and I love talking money and providing hope. Just set up a 30-minute call with me and I’ll listen to your situation and help you determine what needs to happen. My guarantee is if you don’t make progress, you get your money back. I promise the investment in coaching will give you payback many times over.