Debt sucks. Nobody likes debt except bankers. Payments take away from your ability to do what you want!

How am I supposed to splurge on chocolate milk if I have collectors knocking at my door?

There are major two schools of thought on paying off debt and we’ll look at them here. If you’re more of a video learner, check out the video I posted this morning on my YouTube channel!

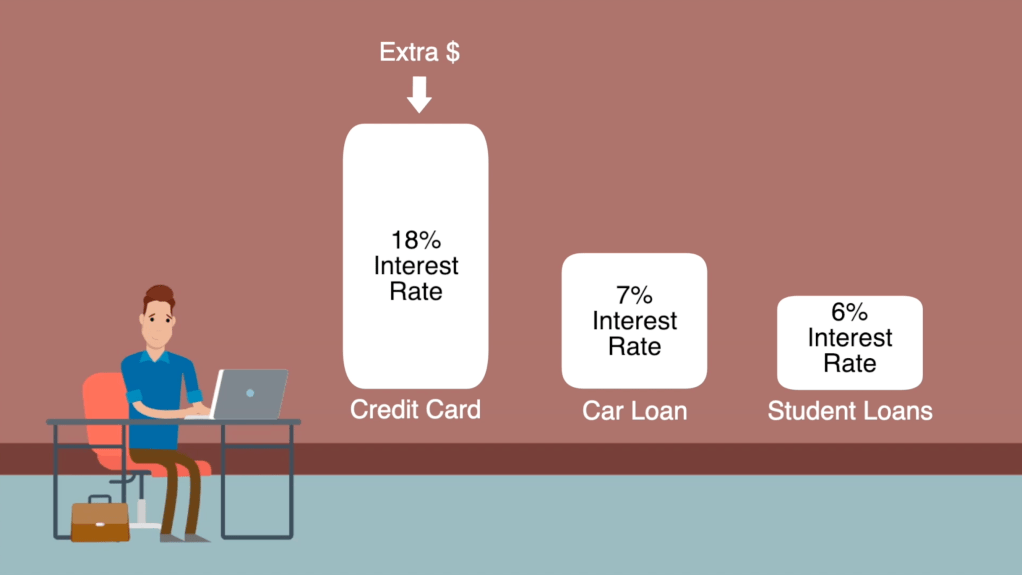

Method 1: Highest Interest Rate First

The first school teaches that to make the most sense, you should line up your loans from highest to lowest in interest rate and then pay off the highest interest rate loans first and move down the line. This’ll get rid of the loans that will cost you the most in the long run.

Obviously you pay the minimum on the rest of your loans as you pay down the highest interest rate loan. This is method is more mathematically based.

Method 2: Lowest Principal First (The Debt Snowball)

The second school teaches the method that is more momentum based. It’s called the debt snowball method.

Did you ever play in the snow as kids and make your own snowman?

I suppose this example might exclude you Southerners..

You take a small snowball, rolling it across the lawn (picking up every sad autumn leaf) until it gets big enough for the snowman’s body? It works because as you roll it, the snowball picks up more and more snow, making it get bigger and bigger.

The debt snowball works just like this.

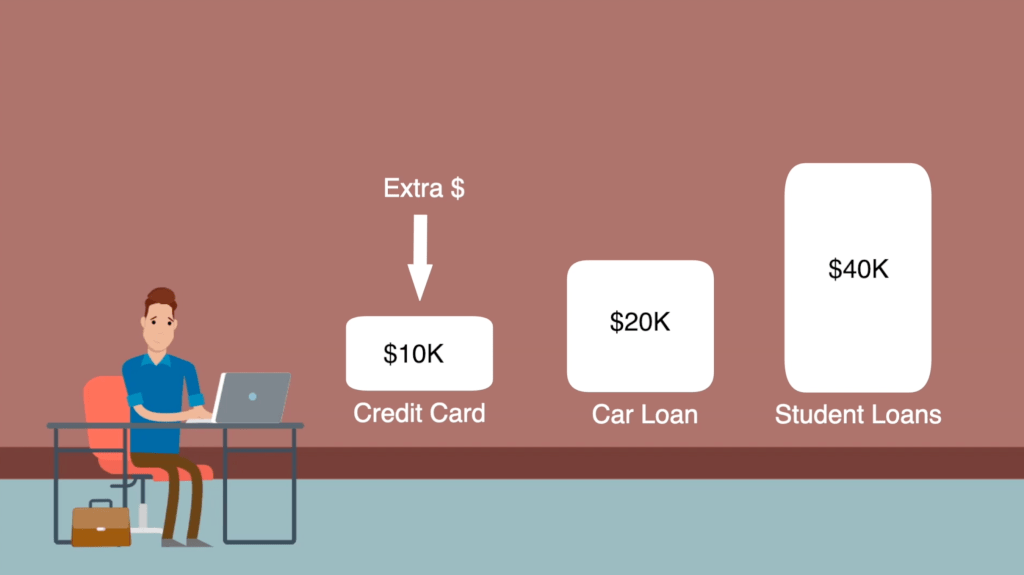

Line up the debts you have smallest to largest regardless of interest rate. EVERYTHING not including your mortgage (because this goes in Baby Step 6). We’re talking phones, credit cards, bank loans, student loans, car loans, cat loans, whatever. Then you’re going to pay the minimum on each debt every month.

Anything left over (and I mean anything) is going to go straight to paying off that smallest debt. If you find a dollar at the office, that goes to paying off your smallest debt.

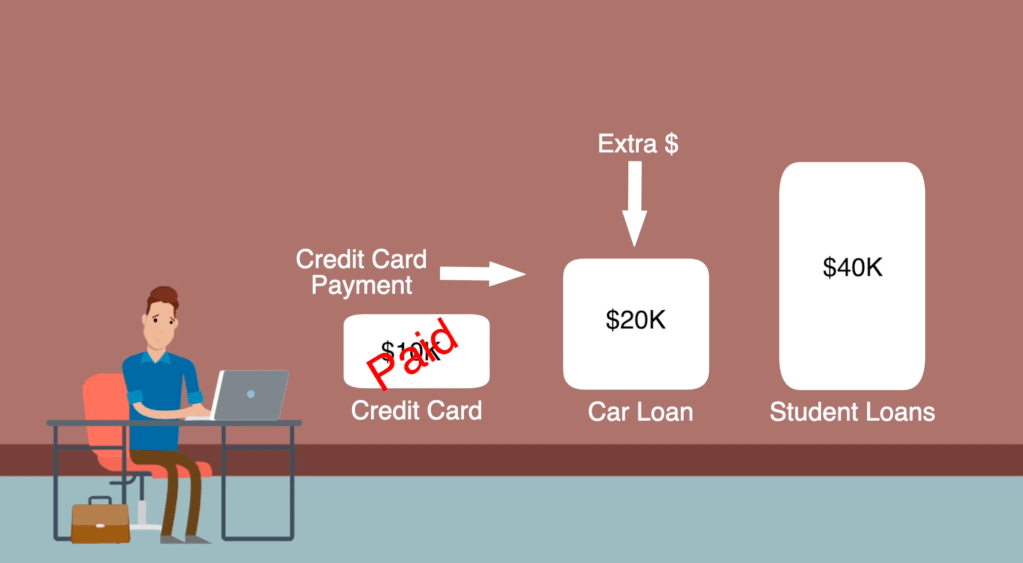

Once you get that paid off, you move onto the next one. This time you’ll have more money to throw at the second smallest debt because you’ve already paid off the smallest.

Once you get that paid off, you move to the third smallest debt and take the money you were using to pay off the first two to pay off the third.

Each loan you pay off, you gain more momentum. It makes it easier to pay off that large loan because you’re building your cash flow up as you rid yourself of those smaller loans. Then you’re debt free!

Let’s Compare Both Methods

Method 1: The pro of the first method is that it will save you money because you’re paying off the high interest loans first. The con — it’s harder to push yourself in your debt payoff when the debt is so large that it’s hard to see past it.

Now, as in the case of our above example with pictures, the highest interest rate loan might be the smallest loan. But in many situations, this is not the case. Sometimes the highest interest rate loan will be the largest, but it’s then that it may be more difficult to muster the motivation to pay off the largest loan first.

Method 2 (The Debt Snowball): The pro of the debt snowball is you get to build momentum through your debt payoff. It’s easier to start paying off the small debts first and continue the process. It’s motivating to get rid of a payment even if it is a small one! The con – it doesn’t get rid of the highest interest loans first necessarily. You might pay more in interest.

My Preference

Personally, I believe momentum is far more important in this case. Sure, you might save money on high interest loans but that only does you any good if you have the discipline to pay off the loan.

And in the grand scheme of things, if you are working your butt off to pay off your debt as quickly as possible in 2021, you’re actually not going to lose that much money in interest by using the debt snowball method.

There isn’t a magic trick to paying off debt. You just have to work hard, control your spending, and hit your debt payments with all you’ve got. You signed up for it, now get rid of it.

Debt Consolidation?

What about debt consolidation? I mean, you could. It is an option and many people do benefit from it.

Though it might help make payments less confusing and get you a lower interest rate overall, you need to get rid of your debt ASAP. Paying it off with the gazelle intensity that Dave Ramsey talks about is the best way for you to knock it out.

When you pay off debt quickly, debt consolidation really doesn’t do you much good. For one, there might be a fee involved. Two, you might not save that much in interest given you’re paying your debt off so quickly. Three, you lose your ability to gain momentum in your debt payoff because now you have one big debt instead of many small ones.

Again, I get it, the debt snowball isn’t the mathematically correct way to do things. I am an engineer by trade so I get the math argument.

But as Dave Ramsey says, if you were doing math, you wouldn’t be in this mess in the first place. Talk about some tough love! This applies to the vast majority of debt circumstances. I understand some situations don’t apply like with many types of medical debt when there’s no other options.

How Do We Get Rid of Debt Faster?

Okay okay, we’re paying off debt fast and building momentum but how do we pay it off even faster?

Get another job, snag some overtime hours, deliver groceries, drive for Uber, start a side hustle, hit the like button to help my blog. Your income is your greatest wealth building tool which means it’s also your greatest debt-destroying tool. Increase it and you have more to work with.

Conclusion

This debt snowball is a proven method that Dave Ramsey teaches in order to help people get out of debt and it’s what we’re taught as financial coaches. And millions have become debt free this way. Don’t take my word for it. Take the word every person who has gotten rid of their debts by this same method.

So I pose this question to you. If you have debt, how is your debt payoff going? Which method are you using and is it working?

Comment below and let me know! I’ll respond to every one.

Like what you read? Give me a follow in this little box below.

Are you overwhelmed by debt and feel like there’s no way out?

I can help! I’m a financial coach trained by Ramsey Solutions to guide people in their financial lives. Set up a free consultation below and I’ll listen to your situation and guide you on the right steps forward. First session is completely free and there’s no commitment.

Money doesn’t have to be confusing. You can be the master of your own finances. But you have to start today.